The Devil is in the Details: Uncovering the Secrets of Insurance Premium Calculation

Evolution of insurance pricing

Gone are the days of simplistic motor insurance premium calculation methods where agents relied solely on a paper-based claims history and limited factors. Today, the determination of premiums has become a sophisticated balancing act for actuaries and pricing specialists seeking the optimal combination of affordability, market appeal, and profitability.

In 2022, the market was valued at a staggering $783.7 Billion, which is more than 13% in relation to the global P&C and Life insurance market, and it is projected to reach an even higher value of $1,282.1 Billion by 2028. Clearly, the motor insurance is still ever-growing huge market, although the autonomous cars are on the horizon. It is vital to become aware of insurance premium calculation approaches, which is what we aim in this article.

What exactly is the motor insurance premium?

Motor insurance premium is the amount of money an individual or business must pay to an insurance company in exchange for a vehicles’ or drivers’ insurance protection against contingent events. The premium is typically based on many factors starting from most common as the type and age of the vehicle, the driver's driving history, and ending with sometimes unobvious, like car height or length.

In the further part of the article, we will focus only on personal lines in motor pricing.

What does insurance premium consist of and how is it calculated?

The premium paid by the customer for the policy is the product of months of the extensive work of pricing actuaries and analysts. The process of its creation is complex and consists of many parts.

Components of the premium:

- Actuarial cost

- Fixed cost

- Variable cost

- Profit margin

- Discounts

- Other factors

Actuarial cost

The primary component of the insurance premium is the actuarial cost, also known as the risk cost. In motor insurance, this refers to the estimated financial loss that the insurance company may experience because of providing coverage for a specific vehicle. This includes the potential costs of paying claims related to accidents or other incidents involving the insured vehicle.

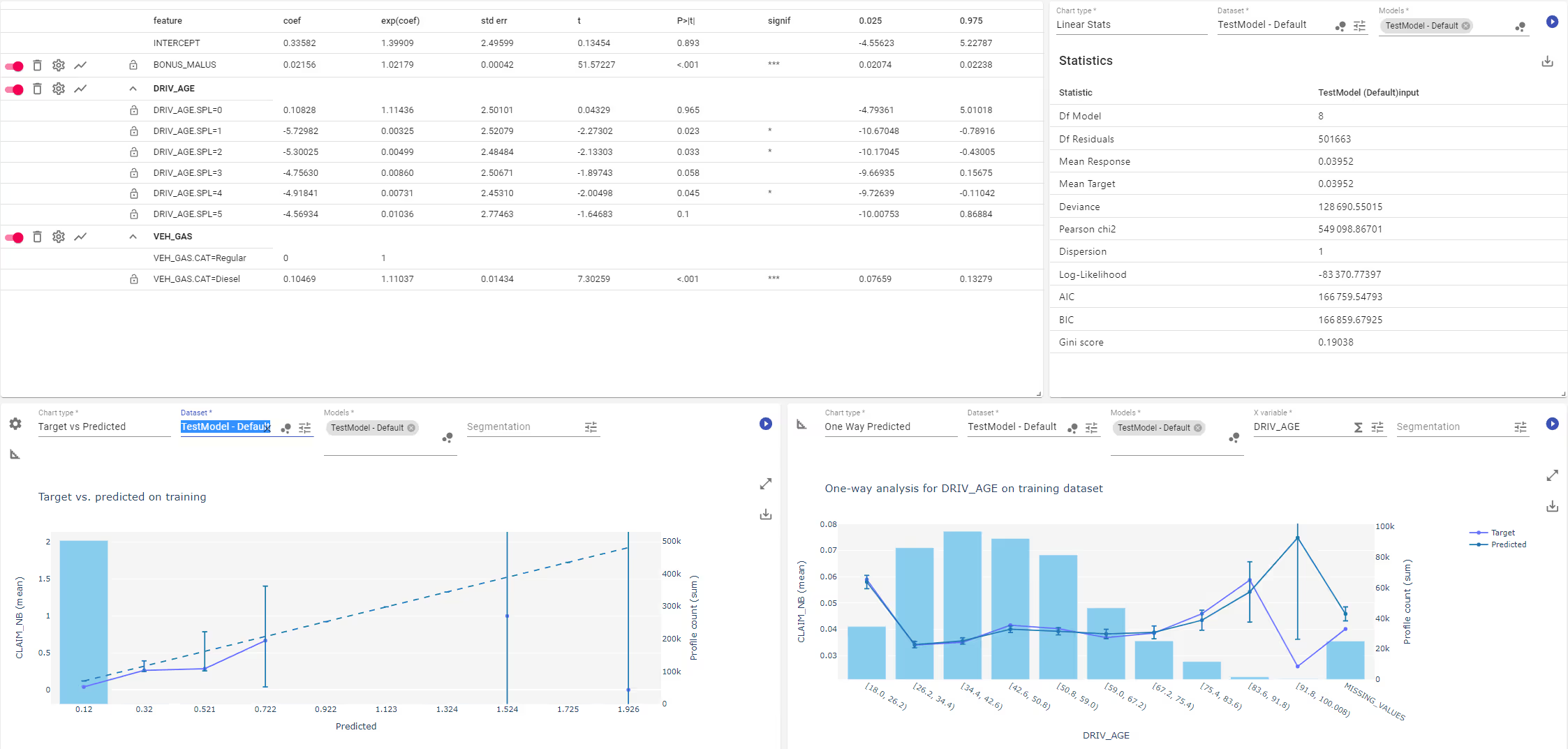

Calculating pure premium in motor insurance can be done using various methods, but one of the most widely used and preferred methods are Generalised Linear Models (GLM). This is primarily because of their ease of use and straightforwardness in interpreting the results. A popular approach within this method is to construct a frequency-severity model, where frequency represents the number of claims and severity represents the average cost of those claims.

Other more advanced methods such as Random Forest or Gradient Boosting Machine can give better predictive results than GLM but are much more difficult to interpret.

[In Quantee platform, Users have 3 modelling modes to choose from: Configurable GLM/GAM, Configurable ML and Automated ML.]

Fixed cost

In addition to the actuarial cost, the premium includes fixed expenses, usually understood as cost of policy maintenance. These are costs that remain constant regardless of the change in the business volume. The main components of these expenses are office maintenance, remunerations, loan repayments and licence fees.

Variable cost

Besides fixed costs, an insurance company also incurs variable expenses associated with the sale of policies, such as commission payments to insurance intermediaries, including agents, brokers, and online sales channels. These commission rates can vary widely, depending on factors such as the size and experience of the intermediary, the number of policies sold, the total premium written, and the tenure in the market.

Profit margin

Like any business, insurance companies aim to generate a profit. To achieve this, they add a margin, or underwriting profit, to each premium they charge. The size of this margin can vary depending on the company's business strategy. A company that wants to attract many customers may opt for a lower margin and offer more competitive premiums, while a company that prioritises profit may choose to increase the margin and charge higher premiums but may acquire fewer clients as a result.

List vs street prices

List price refers to the premium determined by the actuary, while street price is the actual premium offered to the client, which can be lower due to discounts offered by agents. By offering discounts, agents can better tailor the offering and convince undecided customers while sacrificing some of the company's margin. Effective discount allocation and skilled salesmanship might result in not only higher conversion and retention rates but also improved profitability for the insurance company. Pricing actuaries try to predict the agent discounts to correctly estimate financial results for sold products such as loss ratio. Discounts can be calculated in several ways, such as a simple percentage reduction, or through more complex models that take into account factors such as the probability of giving a discount and the amount of the discount for specific segments of customers.

Other factors

Like in many industries, customers often prefer to pay for their insurance premiums in instalments, especially in the case of high premiums. However, this type of payment plan poses a greater risk of non-payment for the insurer. As a result, many insurers will charge a higher premium for instalment plans, with the increase in premium becoming greater as the number of instalments increases.

Pricing insurance products involves not just assessing risk, expenses, and discounts, but also adapting to a dynamic environment. Taking competition into consideration is crucial and is a part of behavioural pricing. The two key approaches in this type of pricing are:

- building demand models that have the competition information inside price elasticity,

- building best price model that will be an input to demand model.

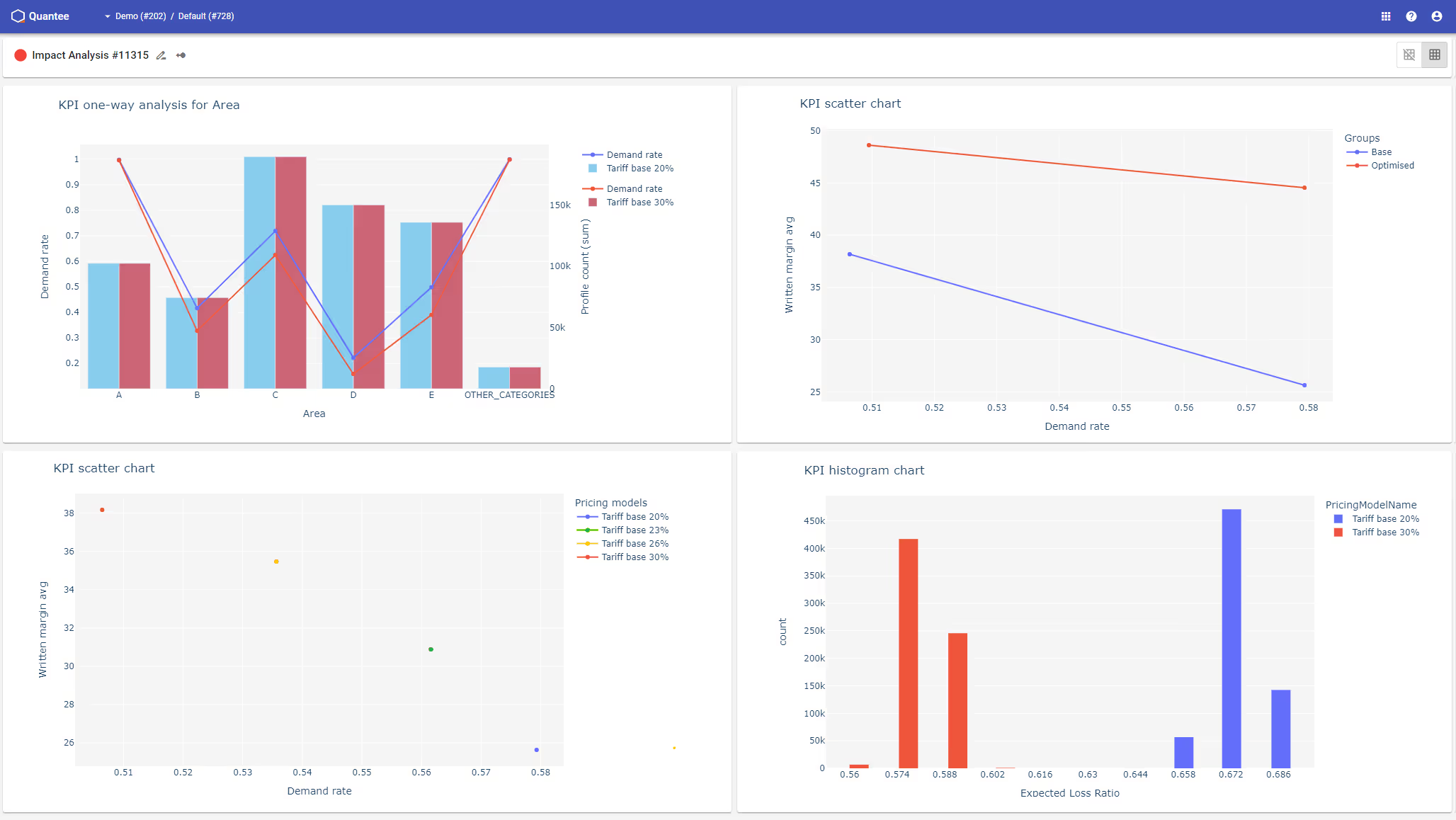

[In Quantee platform, it is quite easy to create and measure KPIs e.g., using charts.]

Regulations and the law

It is important to note that insurance companies are subject to certain limitations when it comes to setting premiums. For example, in the UK, a practice known as “price walking” was prohibited in 2021. This refers to the practice of offering a lower premium to new customers compared to renewal customers within the same segment. This is a regulation imposed on insurers to ensure fair pricing and competition.

The second example is the prohibition in the EU of using gender as a variable in models. Although this variable can differentiate the risk, insurers are not allowed to use it.

What is also worth mentioning is the solvency of insurance companies. Every insurer must be solvent, therefore the data made available to the regulators should be clear and accurate. They need to operate in a fair and ethical manner.

Transparency towards customers is also an important topic. Policyholders have the right to understand the reasons behind any increase or decrease in premium values compared to the previous year. Providing explanations for these changes helps policyholders to understand the factors that contribute to their insurance costs and can promote fairness in the market.

Final remarks

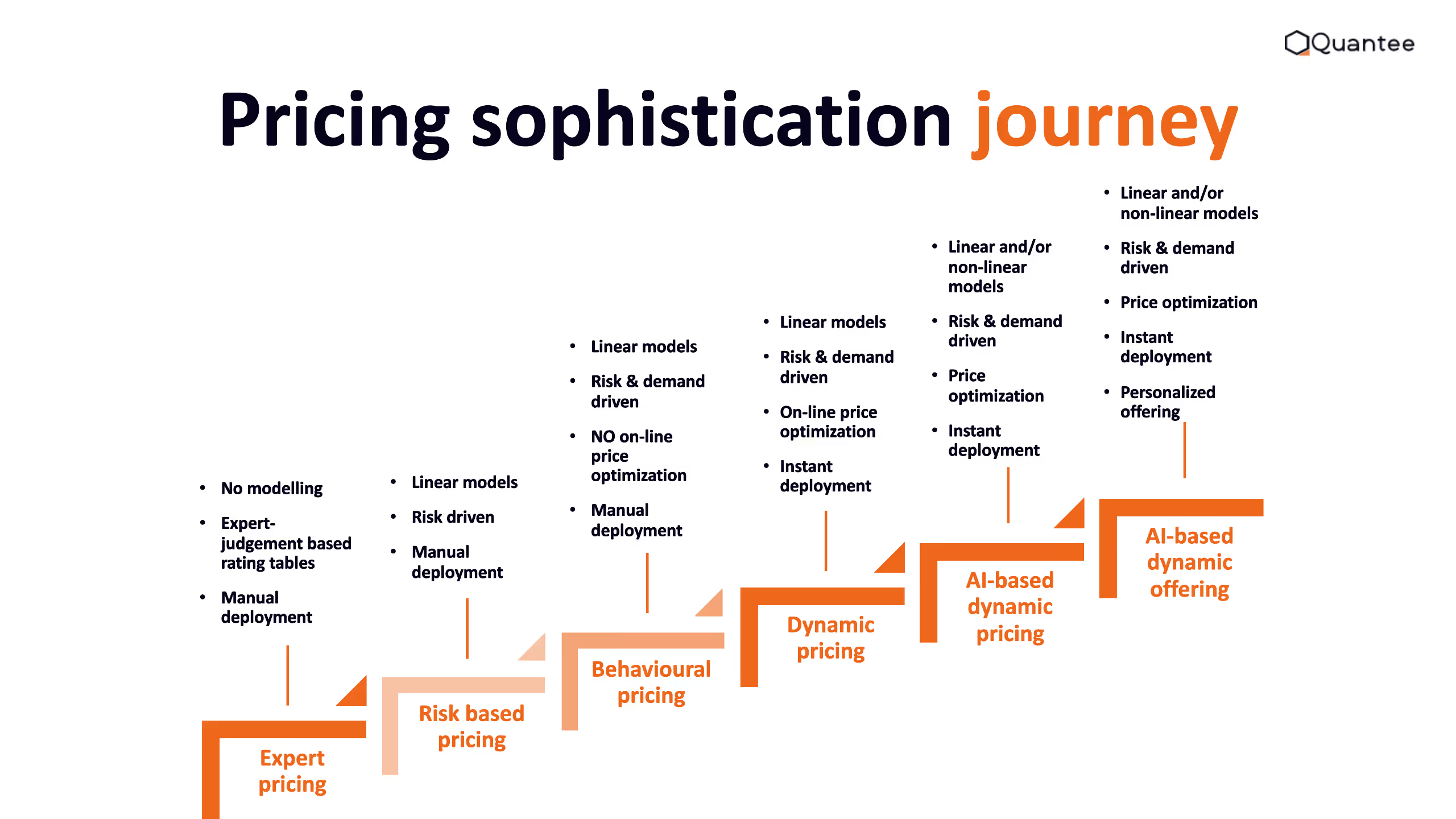

The insurance market is constantly developing very strongly. Pricing models are becoming increasingly advanced and tailored to a specific customer. Achieving such a level sometimes requires the use of e.g., propensity-to-buy models or rules. It is a part of behavioural pricing sophistication.

Determining the insurance premium is a complex and labour-intensive process, as it involves various components and factors. To streamline this process and ensure accurate pricing, utilising specialised software is a valuable asset. Such software not only simplifies the premium determination process but also enables the implementation and management of pricing models in a centralised and efficient manner.

If you are interested in software thanks to which you will be able to not only calculate, combine, but also implement and send the premium to your sales channels in one place - do not hesitate, contact us!

References

https://www.imarcgroup.com/motor-insurance-market

https://www.statista.com/statistics/1192960/forecast-global-insurance-market/